Billbacks, Chargebacks, and Deductions: How the Waterdeep Trading Company Manages Post-Sale Adjustments

In the counting houses and ledger halls of Faerûn, the moment a shipment leaves the warehouse is not the moment profit is certain. Goods may travel safely from Waterdeep to Baldur’s Gate, invoices may be issued without error, and coin may arrive on time. Yet even then, revenue remains vulnerable.

Claims raised after delivery can reshape margins, strain guild relationships, and consume precious clerk hours if they are not properly understood and managed. For the Waterdeep Trading Company, mastering post-sale adjustments is as critical as negotiating the initial contract.

Three terms dominate this realm of delayed accounting: billbacks, chargebacks, and deductions. They are often spoken of together, as though they were siblings born of the same problem. They are not. Each represents a distinct kind of post-sale adjustment, governed by a different authority, triggered by different circumstances, and requiring different responses.

This article clarifies what each term truly means within the context of Faerûn trade. It then presents a complete trade cycle in which all three adjustments appear together, demonstrating how they interact, how they are resolved, and how final revenue is determined when the ledger dust settles.

The Three Types of Post-Sale Adjustments: An Overview

Before diving into the mechanics, it helps to understand what sets these three adjustment types apart at a fundamental level.

A billback is a backward-looking claim rooted in agreed commercial terms. It appears after invoices have been paid because certain contract terms cannot be calculated until a period ends or a threshold is reached. Billbacks are delayed math, not disputes. They reflect volume rebates, retroactive pricing adjustments, or seasonal discount tiers that trigger only after cumulative activity is known.

A chargeback is enforced, not requested. It is a claim imposed by a guild, regulatory authority, or buyer with contractual enforcement power. Chargebacks result from compliance failures, missed delivery windows, failed inspections, or violated quality standards. They are consequences, not conversations.

A deduction occurs at the moment of payment. The buyer remits less than the invoice total and provides a reason for the shortfall. Unlike chargebacks, deductions are not enforced by an external authority. Unlike billbacks, they are not delayed. They arrive as unresolved claims that must be investigated, accepted, rejected, or recovered through evidence and negotiation.

The core distinction lies in authority, timing, and resolution. Billbacks are contractual and anticipated. Chargebacks are punitive and enforced. Deductions are disputed and require proof.

Understanding these distinctions protects clarity, enables root cause analysis, and ensures each type of problem receives the appropriate response.

What Is a Billback?

A billback is a backward-looking claim rooted in agreed commercial terms. It typically appears after invoices have already been issued and, in many cases, already paid.

In simple terms, a billback says: the payment was correct when it happened, but the contract now says the coin is owed back.

Billbacks are contractual, not operational. They do not suggest failure, damage, or error in the delivery process. They exist because certain terms cannot be calculated at the moment of invoicing. They require completion of a period, achievement of a threshold, or confirmation of a total before the adjustment amount becomes known.

Common Billback Situations in Faerûn Trade

A buyer agrees to a quarterly or annual volume rebate. Early invoices are paid at full price. Once the total volume is confirmed at period end, the buyer claims the rebate value back through a billback.

A trade agreement is applied late or updated retroactively by the guild authority. Prior invoices must be adjusted to align with the corrected pricing structure.

A seasonal discount tier is triggered only after cumulative purchases cross a defined threshold. The billback captures the retroactive discount on earlier transactions.

Billbacks are delayed math, not disputes. They reflect agreements that unfold over time rather than errors that require correction.

Why Billbacks Matter

Billbacks affect revenue timing and margin accuracy. If they are not tracked separately from gross sales, early profitability appears higher than it actually is. Quarterly reports may show strength that erodes by year’s end.

For the Waterdeep Trading Company, billbacks are forecast, accrued, and settled deliberately. They are not surprises. They are anticipated consequences of contract design. Tracking them separately ensures that reported profit remains honest and that pricing decisions reflect true net revenue rather than inflated invoice totals.

What Is a Chargeback?

A chargeback is enforced, not requested.

It is a claim imposed by a guild, regulatory authority, clearinghouse, or a buyer with contractual enforcement power. Once a chargeback is issued, the seller cannot negotiate, dispute, or decline it. The adjustment happens.

In Faerûn, chargebacks often arrive bearing guild seals, magistrate writs, or official dock stamps. Coin may already be withheld or reclaimed before the seller even receives notice of the event that triggered it.

Common Chargeback Situations in Faerûn Trade

A shipment fails a mandatory guild inspection at a port or border crossing, triggering a fixed penalty specified in trade law or charter.

Required certification is missing, expired, or invalid at the point of delivery, resulting in mandatory compliance surcharges.

A delivery misses a contractually protected delivery window, such as a festival provisioning deadline or a military supply commitment. The late arrival activates a penalty clause.

An item violates labeling, packaging, or quality standards set by a regional guild or authority, and the violation carries a predefined financial consequence.

Chargebacks are consequences, not conversations. They represent the financial cost of non-compliance or operational failure as defined by the external authority.

Why Chargebacks Matter

Chargebacks highlight risk and process breakdown. They point directly to routing decisions, compliance gaps, quality control weaknesses, or timing failures that need immediate correction.

The Waterdeep Trading Company tracks chargebacks separately from other adjustments, enabling them to be analyzed as operational signals rather than dismissed as pricing noise. A pattern of chargebacks from a particular route, warehouse, or inspector suggests a systemic problem that must be addressed before it becomes ruinous.

What Is a Deduction?

A deduction occurs at the moment of payment.

The buyer receives an invoice but remits less than the full amount and provides a reason, claim, or explanation for the shortfall. Unlike a chargeback, a deduction is not enforced by an external authority. Unlike a billback, it is not delayed until the end of the period. It simply arrives, unresolved, sitting in the ledger as an open question.

A deduction is the buyer saying, “We believe you owe us this coin, and we are keeping it until you prove otherwise.”

Common Deduction Situations in Faerûn Trade

The buyer claims a shortage in the shipment or asserts that the invoice overstates the quantity delivered.

The buyer alleges damage, spoilage, or quality defects discovered upon receipt.

The buyer disputes packaging errors, missing documentation, incorrect labeling, or broken seals.

The buyer disagrees with the price charged, citing a prior quote, promotional rate, or misunderstanding.

Some deductions are valid. Some are partially justified. Some are entirely wrong. The problem is that deductions arrive as claims rather than proven facts. They must be investigated.

Why Deductions Matter

Deductions require time, evidence, and judgment. Ignored deductions quietly become losses. Mishandled deductions damage trust and invite future abuse.

At the Waterdeep Trading Company, deductions are treated as cases, not write-offs. Each one is assigned to a clerk and supported by dock records, inspection notes, and contract terms. Each one must be accepted, rejected, or recovered through negotiation or evidence.

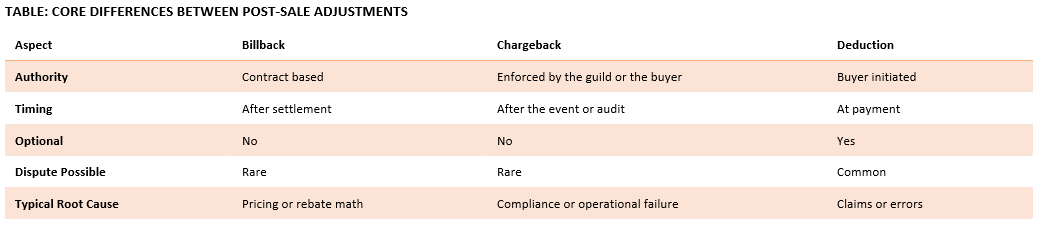

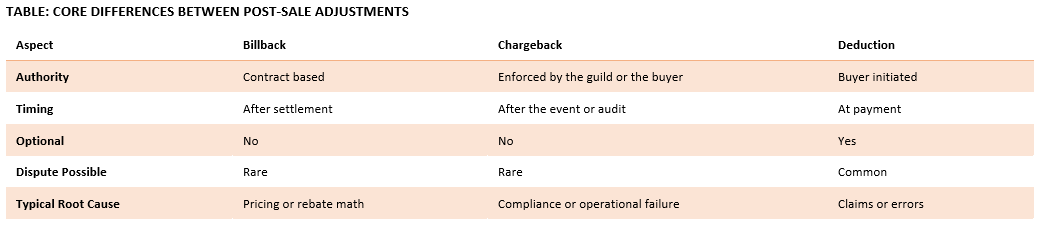

Core Differences That Matter

Understanding the distinctions between these three adjustment types is essential for accurate margin analysis, accountability, and corrective action. The table below summarizes the key differences that separate billbacks, chargebacks, and deductions.

Keeping these three adjustment types separate in the ledger protects clarity, enables root cause analysis, and ensures that each type of problem receives the appropriate response.

Worked Example: Billbacks, Chargebacks, and Deductions in a Single Trade Cycle

To demonstrate how these three adjustments interact in practice, the following example walks through a complete trade cycle involving the Waterdeep Trading Company and a regional tavern chain operating across the Sword Coast.

A quarterly supply contract governs pricing, quality standards, delivery timing, and volume-based incentives. Over the course of the quarter, all three adjustment types appear. The example shows how each one arises, how it is handled, and how final net revenue is determined.

Step 1: The Original Sale

The tavern chain places an order for 100 crates of Harbor Brown Ale, a popular regional brew produced in Waterdeep and distributed along coastal trade routes.

The relevant contract terms are as follows:

- Base price is 18.00 FSD per crate.

- A volume rebate of 2.00 FSD per crate applies retroactively if quarterly purchases exceed 300 crates.

- Delivery must occur within five days of dispatch to avoid penalties.

- All shipments must pass guild quality inspection at the destination dock.

- The invoice is issued, and the buyer receives the goods in good order. Payment is made in full.

The buyer receives the goods and pays the full amount of 1,800.00 FSD without issue.

Step 2: A Deduction Appears

On a later shipment within the same quarter, the buyer remits only 1,760.00 FSD against an invoice total of 1,800.00 FSD. Enclosed with the payment is a note claiming that two crates were damaged upon arrival.

The claimed value of the damage is 40.00 FSD, representing two crates at 20.00 FSD each after accounting for partial salvage.

This creates an open deduction in the ledger that requires investigation and resolution.

The deduction is logged and assigned to a trade clerk for review.

Step 3: Deduction Investigation and Resolution

The clerk retrieves dock records, inspection notes, and delivery logs from both the Waterdeep warehouse and the destination tavern. The evidence is evaluated.

One crate shows verified damage, confirmed by a guild inspector’s seal, noting a cracked barrel and spoiled contents.

One crate damage claim is unverified. No inspection record supports the claim, and the delivery manifest shows no notation of damage at receipt.

Based on this evidence, the Waterdeep Trading Company makes the following resolution:

- 20.00 FSD accepted as a valid damage claim.

- 20.00 FSD rejected and recovered from the buyer through a corrective invoice.

The following table shows how the deduction was resolved.

The rejected portion is recovered through negotiation, and the buyer acknowledges the error. Trust is preserved.

Step 4: A Chargeback Is Issued

Later in the quarter, a shipment scheduled for delivery during the Shieldmeet Festival arrives one day late due to a caravan delay caused by weather along the Coast Road.

The Brewers and Distillers Association reviews the delivery logs and determines that the late arrival violated the festival provisioning clause in the regional supply charter. A fixed penalty is issued.

The amount is 75.00 FSD. The chargeback is enforced and non-negotiable.

The chargeback is recorded as a compliance failure and triggers an internal review of routing reliability during high-stakes delivery windows.

Step 5: A Billback Is Calculated

At the end of the quarter, total purchases are tallied. The tavern chain has purchased 320 crates of Harbor Brown Ale across multiple shipments.

The 300-crates volume rebate threshold has been exceeded. According to the contract terms, a 2.00 FSD rebate per crate applies retroactively to all 320 crates purchased during the quarter.

The total billback owed to the buyer is 640.00 FSD.

A credit note is issued to the buyer, and the billback is applied against the next invoice or refunded directly, depending on the buyer’s preference.

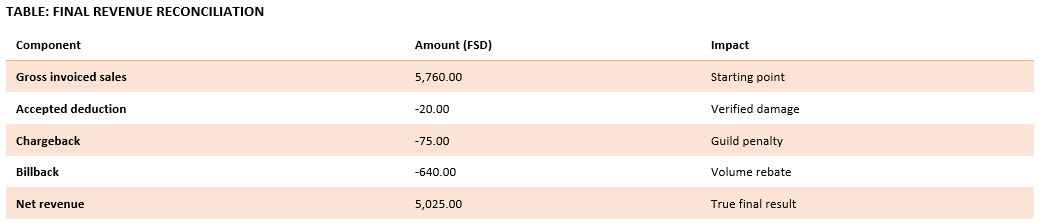

Step 6: Final Net Revenue Reconciliation

The following table shows the final net revenue after all adjustments have been applied. It begins with the gross invoiced sales for the quarter and applies each adjustment in sequence, showing the cumulative impact on revenue.

What This Example Reveals

The deduction tested the strength of proof and the quality of trust between the Waterdeep Trading Company and the buyer. It required investigation, evidence, and negotiation.

The chargeback exposed operational risk and routing vulnerability during critical delivery windows. It triggered process improvements.

The billback reflected the planned commercial terms, which were known from the beginning. It was anticipated, accrued, and executed without surprise.

All three reduced revenue, but for very different reasons. Treating them as interchangeable would obscure the lessons each one offers.

Final Thoughts

Post-sale adjustments are not noise in the ledger. They are signals.

Billbacks speak about agreements and the passage of time. They reflect contract design and the deliberate choice to tie incentives to performance or volume.

Chargebacks speak about discipline and compliance. They reveal gaps in process, timing, or quality control that must be closed before they compound into larger failures.

Deductions speak about trust, evidence, and the friction that arises when expectations and reality do not align. They require investigation and judgment, not passive acceptance.

Understanding and separating these three adjustment types protects coin, preserves reputation, and strengthens the foundation of long-term trade relationships across Faerûn.

Support the AD&D365 Project on Patreon. To grow this world, we’ve launched an official Patreon page where supporters can access exclusive content, tools, and training labs, and even influence the project’s future. Your support fuels more than just development; it expands the guildhall, forges new scrolls, and empowers the next generation of configuration wizards. Begin your journey: https://www.patreon.com/adnd365/

A Grateful Salute to our Patrons. To all those who stand behind the vision, thank you for helping bring this world to life. Our Benefactors, Andre Breillatt and Eryndor Fiscairn‡, your boundless generosity fuels the arcane core of this project. Without your magic, the weave would falter.

Our Apprentices, the spell engines turn, and the training labs thrive thanks to our current Apprentices: Michael Ramirez and Andreth Bael’Rathyn‡. Special thanks to our past Apprentices, whose contributions helped us get here: Ralf Weber, Wendy Rijners, Shashi Mahesh, Julia Tejera, Ben Ekokobe, Tiago Xavier, Naveen Boyinapelli, Marcos Tadeu Wolf, Kathryn Greene, Jason Brown, Mark Christy, and Ashish Singh.

Our Initiates, Jeff Stiles, Harry Burgh, Jesper Livbjerg, Peter Lorre, Gregory Brigden, and Martin Grahm, your commitment marks the start of the deeper path, stepping beyond mere observation into the active shaping of this realm.Our Followers, your steady presence along the journey is a beacon of encouragement: Rusty Cavalier, Eric Shuss, Sunil Panchal, Sarah D. Morgan, Nick Ramchandani, Daniel Kjærsgaard, and Tomasz Pałys.

And our Voyeurs, ever watching from the shadows, clearly intrigued… but not enough to part with a single gold piece. Your silent curiosity is noted and mildly judged.

Want to design your own economic models in Faerûn? Get your own AD&D365 Environment and guides at adnd365.com/start, and request access to the public view of the current database at https://public.adnd365.com – Login npc@adnd365.com, Password N0nPl@yC#822!